Leverage is one of the first concepts that stops traders in their tracks. What is leverage, exactly? The core idea is straightforward: leverage lets you control a larger position in the market than your own capital alone would allow. A trader with $1,000 in their account can open a position worth $30,000 or even $100,000, depending on the leverage ratio their broker provides.

That amplification cuts both ways. The same mechanism that turns a small price move into a meaningful gain can wipe out your balance just as quickly if the market goes against you. Understanding what is leverage — not just the definition, but how it behaves under real conditions — matters more than most traders realise before they experience it firsthand.

This guide from our prop firm covers how leverage works in forex and crypto, what the real-world numbers look like, and how to use it without letting it use you.

What Is Leverage?

At its core, leverage is borrowed exposure. When a broker offers you leverage, they allow you to open a position that is larger than the funds you have deposited. The deposit you put up to open and maintain that position is called margin — leverage and margin are two sides of the same coin.

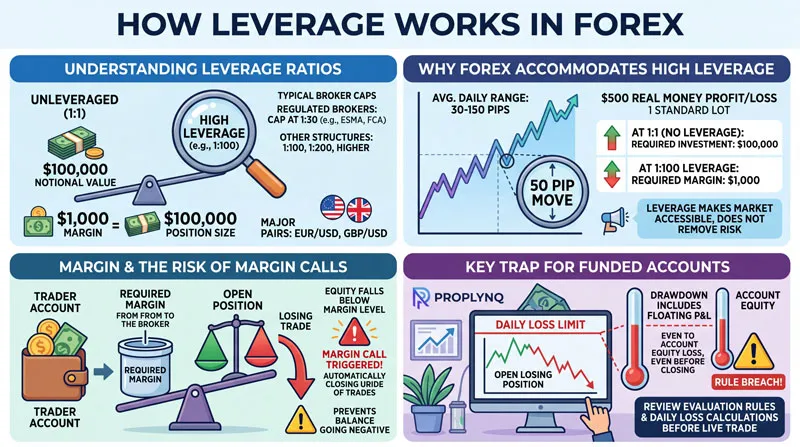

The ratio describes the relationship. A leverage ratio of 1:100 means that for every $1 of your own capital, you control $100 in the market. A 1:30 ratio means your $1 controls $30 worth of exposure.

Leverage does not change the direction of the market, and it does not improve your win rate. What it does is magnify the financial consequence of each pip or percentage-point move. A 1% adverse move on a 1:100 leveraged position erases your margin entirely. The same move on a 1:10 position costs you 10% of it. The mechanism is identical; the scale is what changes.

How Leverage Works in Forex

Forex is the market where leverage ratios tend to be highest. Retail brokers in most regulated jurisdictions cap leverage at 1:30 for major currency pairs — this is the limit set by ESMA for European brokers and mirrored by the FCA in the UK. Brokers operating under lighter regulatory frameworks and prop firms may offer 1:100, 1:200, or higher depending on their structure.

The reason forex accommodates relatively high leverage is the nature of price movement. Major pairs like EUR/USD or GBP/USD typically move in a range of 30 to 150 pips on an average day. At 1:1 — no leverage — a 50-pip move on a standard lot represents $500 in real money. At 1:100, that same 50-pip move still represents $500 per lot, but your margin requirement is $1,000 rather than $100,000. The leverage makes the market accessible; it does not make the underlying risk disappear.

Margin is the collateral your broker holds to keep the trade open. If your account equity falls below the required margin level — caused by a losing open position — the platform may trigger a margin call and close your trades automatically to prevent your balance going negative.

One point that catches many traders off-guard: in most funded account environments, drawdown calculations include your floating P&L, not just closed trades. An open losing position counts against your limit even before it is closed. This is particularly important when using higher leverage, since an open leveraged position can move your equity significantly within a single session. Reviewing the PropLynq evaluation rules before your first live trade — and specifically how the daily loss limit is calculated — removes the most common source of avoidable rule breaches.

How Leverage Works in Crypto

Leverage in crypto operates on the same mechanical principle as forex, but the context is considerably different. Crypto assets can move 5%, 10%, or even 20% in a single session. That volatility fundamentally changes what a safe leverage level looks like in practice.

On centralised exchanges that offer leveraged crypto trading, ratios can range from 2x to 125x depending on the asset and the platform. Perpetual futures are the most common vehicle for leveraged crypto exposure. When you open a leveraged long position on Bitcoin, you are controlling more BTC than you own, with the exchange holding your margin as collateral.

The liquidation price is the critical number to track. If the market moves against your position far enough to exhaust your margin, the exchange liquidates your trade automatically — regardless of whether you believe price will recover. Because crypto swings are larger than forex swings, this can happen within a single candle during volatile sessions.

Funding rates are a second ongoing cost unique to perpetual futures. Longs or shorts periodically pay a rate to the other side based on market sentiment. When the market trends strongly in one direction, funding rates can quietly drain a held leveraged position over hours or days. Understanding these costs is part of sizing any leveraged crypto trade correctly. Traders new to drawdown mechanics in funded environments may also find the breakdown of static vs trailing drawdown useful context — the distinction matters even more in crypto, where volatility can test both limits quickly.

What is leverage Ratios Across Markets — A Comparison

Different markets come with very different leverage environments. The table below shows typical leverage ranges across the major asset classes available to prop and retail traders, alongside the daily volatility context that makes those ratios meaningful.

| Asset Class | Typical Retail Leverage (Regulated) | Typical Prop Firm Range | Average Daily Volatility |

|---|---|---|---|

| Major Forex Pairs | 1:30 | 1:10 to 1:100 | 0.3% – 0.8% |

| Minor / Exotic Forex | 1:20 | 1:10 to 1:50 | 0.5% – 2% |

| Crypto (BTC / ETH) | 2x – 20x (exchange-dependent) | 2x – 20x | 2% – 10%+ |

| Indices | 1:20 | 1:5 to 1:20 | 0.5% – 1.5% |

| Commodities (Gold / Oil) | 1:10 to 1:20 | 1:5 to 1:20 | 0.5% – 1.5% |

The leverage number alone tells you nothing without knowing the typical daily volatility of the instrument. A 1:10 position on an asset that moves 0.5% per day is fundamentally different from a 1:10 position on an asset that moves 5% per day — yet both carry the same stated ratio. The column that actually matters in this table is the last one.

What Leverage Actually Does to Your P&L — A Real Example

Numbers make the concept concrete. Consider a trader with a $5,000 account opening a position on EUR/USD.

Scenario A — No leverage (1:1): They buy $5,000 of EUR/USD. A 1% gain returns $50. A 1% adverse move costs $50. The account is in no danger.

Scenario B — 1:10 leverage: The same $5,000 margin controls $50,000. A 1% gain returns $500 — 10% of the account. A 1% adverse move costs $500, also 10%.

Scenario C — 1:50 leverage: The same $5,000 margin controls $250,000. A 1% gain returns $2,500. A 1% adverse move costs $2,500 — half the account. A 2% adverse move closes it entirely.

The position size is the same in all three scenarios. What changes is the capital efficiency and the per-point risk. EUR/USD has moved more than 1% in a single session many times — it is not a rare event. A 1:50 leveraged position, sized without reference to that fact, is not aggressive trading; it is unmanaged risk dressed up as a strategy.

The question a trader should ask is not what is the maximum leverage available to me? but what position size, given my leverage, creates a loss I can absorb and recover from? Traders who fail funded evaluations most often do so not because the market moved unexpectedly, but because leverage turned a normal losing trade into an account-ending one. The guide on how to pass a prop firm challenge addresses exactly this point — position discipline is what separates traders who pass from those who repeat the evaluation.

Common Leverage Mistakes Traders Make

Leverage amplifies everything — including mistakes. These are the patterns most consistently seen in traders who lose funded accounts or blow retail accounts early.

Treating the maximum as the default. Most brokers and prop firms publish a maximum leverage ratio, not a recommended one. Using the ceiling as your starting point is one of the most reliable ways to end an account quickly. The ceiling exists as an option, not a suggestion.

Ignoring drawdown limits when sizing positions. A funded account with a 5% daily loss limit and 1:100 leverage creates a situation where a single poorly sized trade can breach the daily limit in one move. The leverage ratio is meaningless without reference to the loss limit you are operating within. Those two numbers — leverage and drawdown — need to be thought about together, not separately.

Adding to a losing leveraged position. Averaging down works in low-leverage, wide-stop environments with patient capital. In leveraged trading, each addition multiplies the exposure and accelerates the path to liquidation. The position either recovers or it ends the account — there is very little middle ground when leverage is involved.

Confusing lot size with leverage. Two traders can use identical leverage but carry completely different risk exposure if they are trading different lot sizes. Leverage sets the multiplier; lot size determines the dollar value per pip movement. Both variables need to be set deliberately, not just one of them.

Using high leverage around major news events. Events like Non-Farm Payrolls, central bank rate decisions, or CPI releases generate spread widening and price gaps. Stop-loss orders can be skipped entirely in these conditions — the market gaps past them without triggering the order at the expected price. High leverage during news events is one of the most reliable routes to a margin call that had nothing to do with your analysis being wrong. Before trading around scheduled releases, it is worth understanding how news trading in forex works at a mechanical level, particularly how spreads behave in the minutes before and after impact.

Choosing the Right Leverage Level for Your Strategy

There is no single correct leverage level for every trader or strategy. The right level depends on how you trade, what you trade, and the rules of the environment you are trading in. Working through these considerations before setting your leverage provides a practical starting framework.

- Maximum loss per trade: What percentage of your account balance are you willing to lose on a single trade? Your position size — not your leverage — should enforce that limit. Leverage just determines how many units you can access per dollar of margin.

- Instrument volatility: What is the average daily pip range or percentage move of the instrument you are trading? Higher volatility requires lower leverage to keep individual trade risk constant across sessions.

- Drawdown limit: If you are trading a funded account, what is the maximum drawdown allowed — and is it calculated on balance or equity? Equity-based drawdown, which includes open positions, tightens the real-world limit further than traders often realise.

- Stop placement: Wide stops require lower leverage. A 100-pip stop on a 1:100 position in a $10,000 account is a $1,000 risk — 10% on one trade. The same stop at 1:10 is $100.

- News and overnight exposure: Are you holding positions through scheduled news events or overnight? Both scenarios introduce gap risk that leverage magnifies significantly.

A scalper using very tight stops on major pairs in the London or New York session can often justify higher leverage, because their maximum per-trade loss stays controlled by design. A swing trader holding positions over multiple days should use considerably lower leverage, because the position remains exposed to overnight gaps and multi-session moves that a stop may not fully contain. The question of which approach suits a prop challenge environment is something the guide on trading styles and prop challenges covers in detail — the interaction between leverage, style, and drawdown rules is not the same for every type of trader.

A conservative starting point for traders new to leveraged instruments: no more than 1:5 to 1:10 for forex, and 2x to 5x for crypto. As consistency improves and position-sizing discipline becomes automatic, there is a measured case for adjusting leverage upward — but only after the underlying edge is proven across enough trades to mean something.

What is Leverage mean in PropLynq challenges

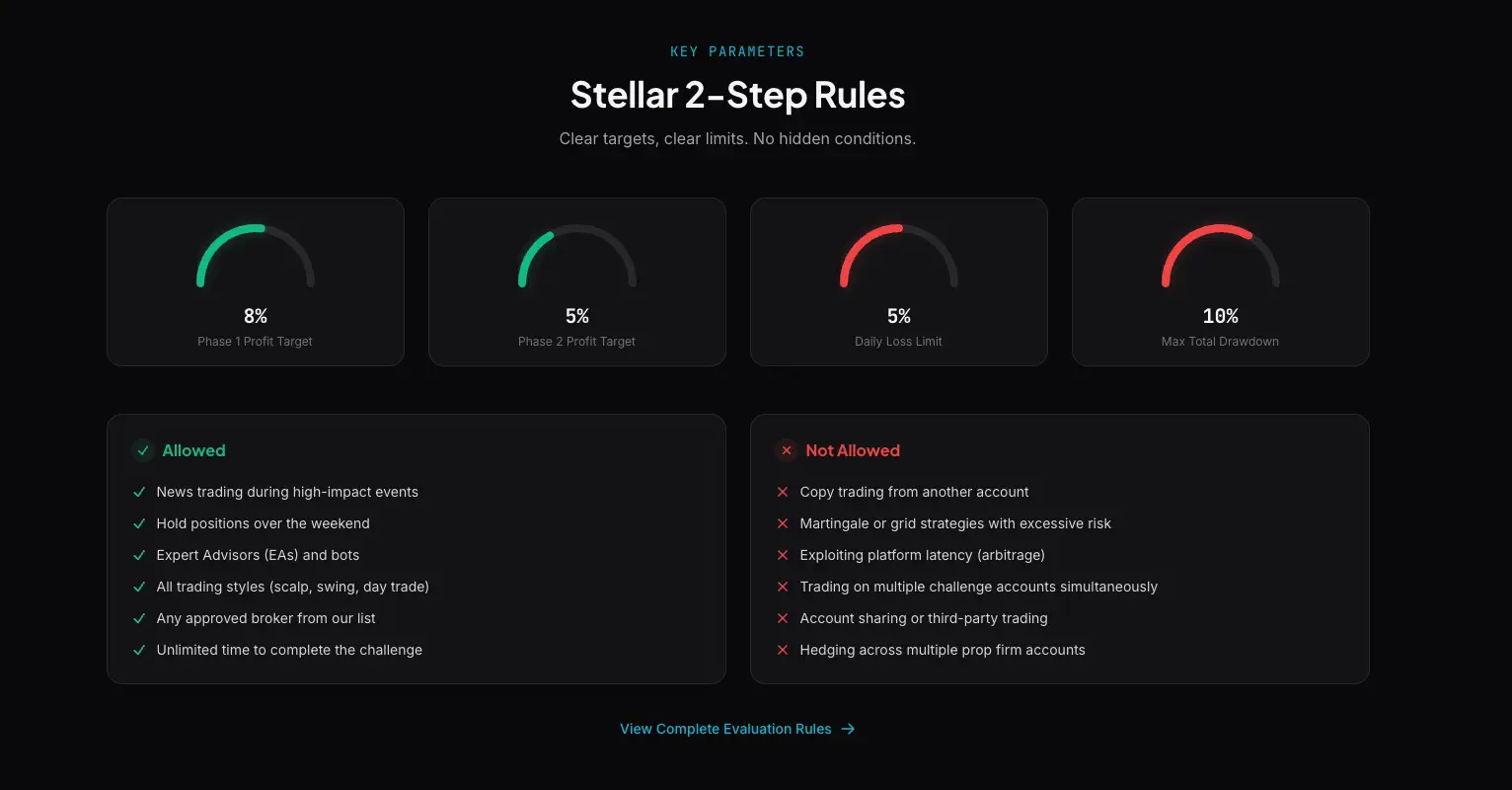

PropLynq’s challenge accounts allow a maximum leverage of 1:100 on the 2-Step Challenge — the platform’s most popular evaluation model. That ceiling gives traders meaningful position-sizing flexibility, but the structure around it is what traders actually need to internalise before they place their first trade.

The 2-Step Challenge operates with a 5% daily loss limit and a 10% maximum total drawdown, both calculated on equity — meaning open floating P&L counts toward the limit, not just closed positions. On a $50,000 account, the daily limit is $2,500 and the total drawdown floor is $45,000. At 1:100 leverage, a single lot of EUR/USD carries roughly $10 of risk per pip. A 250-pip adverse move on a full lot — without a stop — would breach the daily limit on its own. Leverage and drawdown rules are not separate settings to configure once and forget; they are a system that must be treated as a whole.

The BYOB model at PropLynq adds another dimension to this. Because traders connect their own broker account — from an approved list that includes IC Markets, Pepperstone, Exness, and others — the actual leverage available on a given instrument depends on both the PropLynq ceiling and the broker’s own limits for that account type. A trader using a regulated European broker will have a lower effective leverage than one using an offshore broker that offers 1:500 by default. The PropLynq cap of 1:100 acts as the governing ceiling regardless of what the broker would otherwise allow.

Traders who maintain consistent performance scale automatically: after four consecutive months of profitable payouts, the funded account balance increases by 40%, with a path to a maximum allocation of $4,000,000. Reviewing the full structure on the PropLynq trading accounts page before choosing a challenge size helps ensure the account parameters match your actual trading style — not just the account size that looks appealing.

Using Leverage Wisely: The Bottom Line

Understanding what is leverage — not just the textbook definition, but how it multiplies gains, losses, and mistakes in equal measure — is the difference between using it as a precision instrument and treating it as an accelerator with no brakes.

The traders who use leverage well are not the ones who use the most of it. They are the ones who know exactly what each trade does to their account at the leverage level they have set, and who never let that exposure exceed the risk they planned for before the session opened. Leverage is a tool. Like any tool, it is only as useful as the discipline behind it.

Whether you are building a long-term forex strategy, exploring leveraged crypto markets, or preparing for a funded evaluation, the principle holds in every environment: start lower than you think you need to, let your edge prove itself across enough trades, and scale leverage only when your consistency genuinely earns it. If you are ready to apply that discipline under real evaluation conditions, the PropLynq challenge is structured specifically for traders who take position management seriously.